- 83 million Nigerians pushed into extreme poverty, 13 million between 2016 and 2022 •UN projects 401 million population growth by 2050

When President Muhammadu Buhari and stalwarts of the now-ruling All Progressives Congress travelled from state to state canvassing for votes in late 2014 and early 2015, their message was clear: the then government of Goodluck Jonathan had failed on all fronts, especially security and the economy. Nigeria’s development indices were poor and would eventually get worse if Jonathan was not removed, they harped.

Fast forward to seven years after and the indices are not any better rather the situation has worsened. The poor indices are not particularly limited to the not-so-well outing of the current administration. The broader picture lends to an outlook dotted with gloom and imminent catastrophe.

Here is a quick dive into the development indices.

Nigeria’s population, in some quarters, is seen as a significant part of its problem. 216 million people splashed across 36 states and the Federal Capital Territory, experts say, is a big deal. But others argue that the large population can be harnessed and utilised for the good of the country. Those who argue in this regard say the huge population provides a huge market for entrepreneurs.

There is a huge market indeed, but there are fears that the government over the years has not really invested in the critical sectors of the country like electricity, health, education and more. During a presentation at the Nigeria Guild of Editors’ roundtable on data-based national reporting, recently, the Editor-In-Chief of the Africa Centre for Development Journalism, Mr Rotimi Sankore, said the growing population without adequate investment in the critical sectors of the economy is the main threat to Nigeria’s progress.

He explained that Nigeria’s population keeps growing while other development indices do not keep up with the population growth rate. This, he said, is a big threat and should be reversed and lessons learnt from a country like France. France, he noted, had the same population as Nigeria as of 1960 (45 million).

“By 2000, the population of France had gone up by 20 million while Nigeria’s 161 million. Investment in health, electricity, education etc haven’t kept up with population growth. What did they think was going to happen?” Sankore asked.

Nigeria’s population, the UN said, is projected to hit 401 million by 2050 from 216 million this year, transiting through 233 million in 2025, 262 million in 2030, 294 million in 2035, 329 million in 2040 and 364 million in 2045. This great growth is powered by a high fertility rate which is as high as more than 7 births per woman in northern states like Sokoto, Jigawa, Katsina and Bauchi.

The implication is that 80.3 million under-15-year-olds (which is roughly the current population of Germany) are expected to be added to Nigeria’s population by 2030 and an additional 216.3 million (just over the current population of Brazil) under-35-year-olds to Nigeria’s current population by 2050. Another worrisome aspect, experts say, is that Nigeria’s annual population growth rate (2.6 per cent) is more than double the global population growth rate of 1.05 per cent per year.

The projections mean there would be daily births of 21,087, at the least, which translates to a net increase of one person per six seconds, analysis by Sankore shows.

This projected growth, if unbridled, portends serious developmental dangers to Nigeria, especially if there is no commensurate investment in health, education, electricity and other critical sectors. The country dropped three spots to 161 in 2019 from 158 in 2018 among 189 countries in the 2020 Human Development Index (HDI).

The population-poverty-insecurity nexus

For this report, the Sunday Tribune obtained data from the World Poverty Clock and analysed the progress of extreme poverty in the country. The analysis shows that the number of Nigerians in extreme poverty has moved from 70 million in 2016 to 83 million as of August 2022. The progress of poverty has been consistent as it transited through 71 million in 2017, 73 million in 2018, 77 million in 2019, 80 million in 2020 and 81 million in 2021 before reaching the 2022 figure.

This means that between 2016 and 2022, no fewer than 13 million Nigerians — more than the combined number of people living in Qatar, Maldives, Sao Tome and Principe, Gabon, Botswana and Gambia — slipped into extreme poverty. Extreme poverty, for context, means living on an income of less than N1,000 ($2) per day.

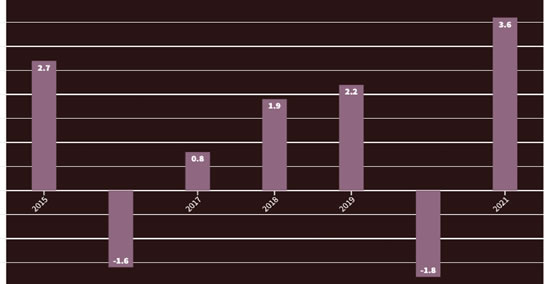

The economic growth data does not really bring a glimmer of hope. Since 2014, the growth has been sluggish, at best, and negative, at worst. Data from the World Bank show that in 2015, Nigeria’s GDP growth was 2.7 per cent. In 2016, it declined massively into the negative region to -1.6 per cent. The next year, it recovered to 0.8 per cent and 1.9 in 2018. In 2019, it was 2.2 per cent but declined again — this time the worst the country had since 1993 — to -1.8 per cent. Last year, it recovered to 3.6 per cent.

In June this year, the World Bank said it had reviewed the 2022 forecast to 3.4 per cent, up from the previous forecast of 2.8 per cent. Simple arithmetics of the data show that from 2015 to 2021, the GDP growth averaged a paltry 1.1 per cent while the population growth kept being stable.

There are implications. Chidi Odinkalu, former chair of the National Human Rights Commission, in a recent article, said “the result is that the supply of public goods is exponentially mismatched against the demand. Absent capable institutions and leadership, the ensuing contest can only be resolved by violence.”

There exists a nexus between exploding population, poverty and insecurity and experts say, that reality bedevils Nigeria today. “Poverty and insecurity are mutually reinforcing, leading to doom spiral,” said Lael Brainard in a paper she co-authored with Derek Chollet on ‘The Tangled Web: The Poverty-Insecurity Nexus’.

Nigeria has faced a myriad of security challenges in the past few years. In the North-East of the country, the Boko Haram terrorists have kept pace for years, driving businesses out of the region. The farmer-herder clashes in the North-West and North-Central regions of the country have unsettled farmers: in May 65 farmers were killed on their farms.

In June 2021 alone, Nigeria recorded over 763 killings. One state alone, Kaduna, in the northwest, officially reported a toll of at least 545 killed and 1,723 kidnapped in the first six months of 2021. The reported ransom economy in the first half of 2021 alone grossed over N10 billion (about $20 million), according to an SBM Intelligence analysis, although the actual sums are believed to be significantly higher. According to a report by The Financial Times, “the kidnapping industry is thriving in Nigeria.”

The herder-farmer clashes have also affected some parts of the South-West. In the oil-rich Niger Delta region, oil installations have been attacked, affecting the country’s production output. In the southeast, a separatist group is constantly clashing with security forces and kidnap-for-ransom has increased.

Nigeria

Deep-cutting implications

In this complex situation, the economy and the everyday Nigerian suffer. The implications of the growing insecurity are such that cut really deep into the economy of the country. It is particularly worrisome given that the country has been bedevilled by poor infrastructure and low public confidence for years.

“The lack of political will to fight violent crimes is the reason why the president put a clannish security architecture in place and it hurts the economy severely”, John Uwaya, a Lagos-based security analyst told the Sunday Tribune.

“The clannish security architecture is forfeiting the benefit of better decisions by people of different cultural backgrounds and perspectives. In fact, a team of Nigerians with different skills, life experiences and cultural backgrounds would leverage each individual’s strengths for national security.”

The implications of the inability of the government to tackle insecurity manifests in the low confidence of investors in the economy, a high mortality rate of businesses and attendant poverty which spreads across the country, Adeola Adenikinju, a professor of Economics and head of the Department of Economics, University of Ibadan told Sunday Tribune.

“This is a major pushback for foreign investors who want to invest heavily in the economy”, he said, noting that neighbouring countries like Ghana are now the preferred destinations where investors are leaving Nigeria for.

“If you are putting your resources in an investment, you have to ensure that you are able to recover your resources in case anything happens,” said Adenikinju. “The issue of insecurity has affected foreign capital flows into Nigeria and some parts of the country are considered to be unsafe and that narrows the kind of investment that will come in.”

In early June, Nigeria’s statistical agency, the National Bureau of Statistics (NBS) released a report detailing a sad decline in capital importation into the country in the first quarter of the year.

The report shows that the total value of capital importation into Nigeria in the first quarter of 2022 was only $1.57 billion, slumping from $2.18 billion in the preceding quarter. It revealed a decrease of 28.09 per cent. The decline was not limited to a quarter-on-quarter basis. When compared to the corresponding quarter of 2021, capital importation decreased by 17.46 per cent from $1.90 billion.

Further analysis of the data shows that there has been a consistent decline in the past few years. In 2019, it dropped from $23.99 billion to $9.66 billion in 2020 and further down to $6.7 billion last year.

The Q1 report shows only six out of the 36 states of the country secured foreign investments — Lagos ($1.12 billion), Abuja ($446.81 million), Anambra ($4.15 million), Oyo ($2 million), Katsina ($0.70 million), and Plateau ($0.04 million).

This shows that even if the problem of insecurity is seen as a national issue, the impacts are local, Dr Emmanuel Nwosu, who lectures on development economics and micro econometrics at the University of Nigeria, Nsukka, told Sunday Tribune.

“Investors do not like to invest in any environment full of uncertainty,” said Nwosu. “Nigeria is an uncertain economic environment for investors.

(Tribune)